Unternavigation

Cost Development and Funding of Health Insurance

Costs issues have been at the heart of political debates on healthcare since the 1960s. Concerns have been raised about the ongoing ‘cost explosion’ on the one hand and, on the other, there have been numerous discussions regarding reforms to healthcare funding.

The Health and Accident Insurance Act passed in 1912 entrusted the cantons with the decision whether or not they wished to introduce compulsory health insurance and thus benefit from federal subsidies. Consequently, health insurance and its funding have developed differently from canton to canton. This situation largely persisted until the full revision of the Health Insurance Act of 1994 and formed the backdrop of debates on funding and cost development in health insurance.

The ‘Cost Explosion’ Debate

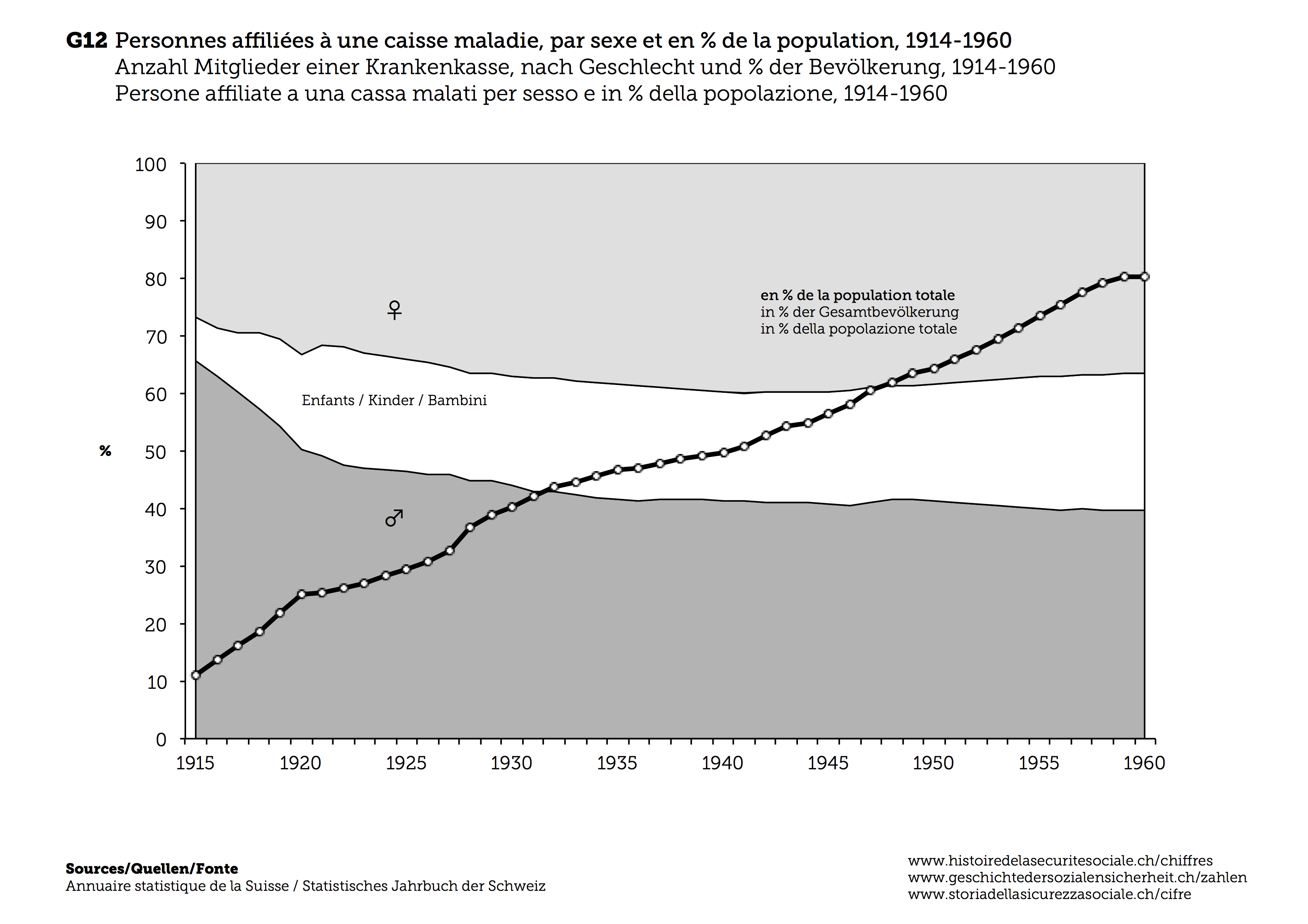

The term ‘cost explosion’ emerged in connection with healthcare in the 1960s. It initially referred to the fact that the rise of healthcare costs was out of step with economic growth since at least the 1950s. Paradoxically, the ‘explosion’ denotes a rather slow trend persisting over decades. The share of healthcare in GDP rose from five per cent in 1960 to seven per cent in the 1980s and ten per cent in 2000. It has since fluctuated between ten and eleven per cent. This ‘cost explosion’ is based on a trend that was politically wished-for and uncontroversial in society for a long time. Switzerland was able to afford an expensive healthcare system during the boom years following the Second World War. Cantonal contributions played a critical role in this system. Cantons began to heavily invest in healthcare in the 1950s through massive expansion to hospital infrastructure and medical services. Furthermore, the demand for health insurance also rose substantially, in part due to the initiative of cantons and cities that gradually improved insurance provision and the reach of mandatory health insurance. The number of insured people doubled between 1945 and 1965. The fraction of the population that was insured rose from around 50 percent in 1945 to more than 80 percent since the mid-1960s (F12). Even without a nationwide health insurance obligation, health insurance covered virtually the entire Swiss population by 1980.

{kind=link}

Healthcare Finances Since the 1960s

Health funds often faced a precarious financial situation in the early post-war period. A growing portion of their business concerned the regulated market of mandatory health insurance. In this case, the authorities ultimately decided on the scope of insurance coverage and the socio-political caps on insurance premiums. They therefore only had a limited capacity to pass rising costs onto premiums. Many funds had already run up deficits during the interwar period as a result of the economic crisis. For structural reasons – namely the lack of structural reforms and stagnating federal subsidies – the difficult financial situation of health funds did not change fundamentally during the early post-war years.

In light of these circumstances, health funds had already called for a significant increase in federal subsidies in the interwar period. The partial revision of the Health Insurance Act of 1964 addressed this concern. Its most important change was a major increase in state subsidies to health funds. These subsidies were now linked to the expenditure trend of health funds in order to stabilize their earnings situation in the long term. The aim was for the Confederation to cover up to 30 per cent of funds’ expenditures. The financing of health insurance took a new direction after 1964. The federal subsidies were gradually increased (by 312 percent from 1966 to 1976, from 193 million to 795 million francs), while the contributions paid by policyholders – in the form of insurance premiums – decreased slightly in comparison (from 68.3 to 67 percent from 1966 to 1976).

However, this development did not last. Once the economy slid into a recession in the mid-1970s and tax revenues receded, the Federal Council enacted a number of emergency measures to limit the burden of health insurance subsidies on the federal budget. Federal subsidies were cut in a linear fashion by ten percent from 1975 to 1976. The proportion of subsidies in health fund earnings was reduced from 16.6 to 14.4 percent between 1975 and 1981. At the same time, policyholders faced higher premiums. The minimum patient deductible was increased from 20 to 30 francs in a bid to compensate for the reduced federal support. The share of costs borne by policyholders rose from 5.7 to 6.7 percent between 1975 and 1981.

For the time between 1980 and 2000, the overall development of the distribution of costs in healthcare between the state, insurance providers and private households can be summarized as follows: the share of costs borne by the state (Confederation, cantons and municipalities) fell from 19 to 15 per cent and from 39 to 32 per cent for self-paying patients, while the costs of insurance (social and private insurance schemes) increased from 40 to 50 per cent.

Literatur / Bibliographie / Bibliografia / References: Alber Jens, Bernardi-Schenkluhn Brigitte (1992), Westeuropäische Gesundheitssysteme im Vergleich: Bundesrepublik Deutschland, Schweiz, Frankreich, Italien, Grossbritannien, Frankfurt ; Sommer Jürg (1978), Das Ringen um die soziale Sicherheit in der Schweiz. Eine politisch-ökonomische Analyse der Ursprünge, Entwicklungen und Perspektiven sozialer Sicherung im Widerstreit zwischen Gruppeninteressen und volkswirtschaftlicher Tragbarkeit, Diessenhofen ; Bundesamt für Statistik (2003), Gesundheitskosten in der Schweiz. Entwicklung von 1960 bis 2000, Neuchâtel.

(12/2015)