Unternavigation

Pension Provision in Numbers

Over the entire 20th century, expenditures for pension funds and AHV (basic old age insurance) accounted altogether for around two thirds of the total social insurance expenditures (F2). The crucial role of old age pensions can mainly be explained by increasing demographic aging over the course of the 20th century (F4).

{kind=link}

{kind=link}

The respective weight of AHV and pension funds in the system of old age provision underwent significant changes during the 20th century. After being introduced in 1948, the expenditures for AHV quickly reached and exceeded the expenditures for occupational old age provision. At the time, the latter only encompassed a minority of wage-earners (around 50 percent in the 1970s). The introduction of the Federal Law on Occupational Provision (BVG) in 1985 reversed this trend: whereas AHV expenditures have since then only increased marginally, pension funds expenditures have doubled.

The strong upward trend in occupational provision can be illustrated by comparing the number of AHV and BVG pension recipients (F5). In 2010, only a little over half of AHV pension recipients received a BVG pension (compared to 30 per cent in 1980). This discrepancy may be traced back to the fact that, for decades, only a minority of wage-earners had access to occupational provision. For instance, twice as many men as women were affiliated to a pension fund prior to the introduction of the BVG (F6). Even after the BVG was introduced, a fifth of wage-earners remained without a pension fund. Women with wages below the BVG entry threshold represented the overwhelming majority (90 per cent) of those affected.

{kind=link}

{kind=link}

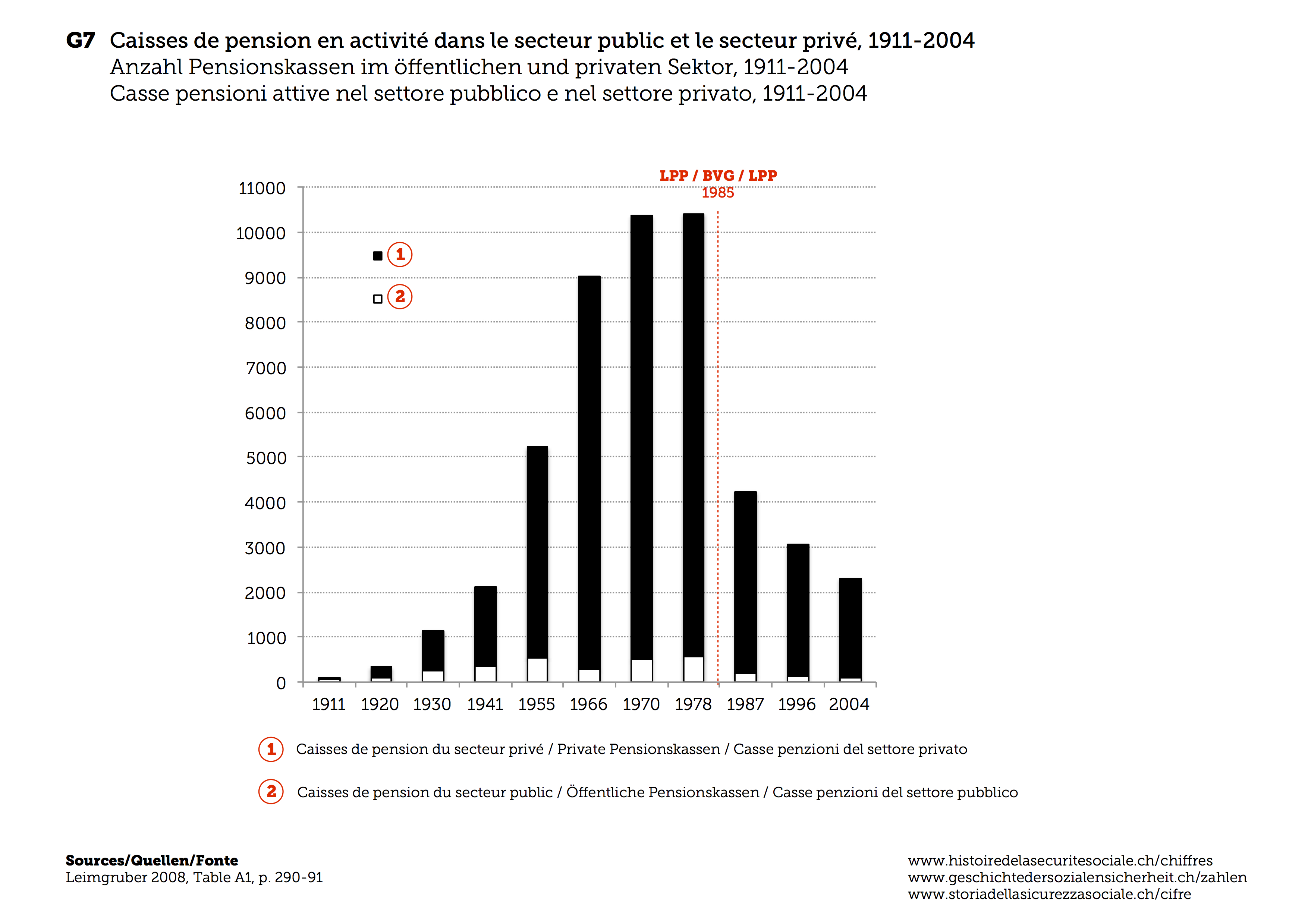

The introduction of the BVG led to a fundamental change in old age provision. The number of pension funds increased ten-fold between 1930 and 1978 (F7): In 1978, more than 10,000 pension funds operated in this domain. This extensive degree of fragmentation was chiefly due to “group insurance” contracts, which resulted in the major life insurance companies serving a very large number of small and medium-sized companies. After 1985, many ‘welfare funds’ unable to meet the minimum requirements of the BVG (in particular regarding benefits levels and eligibility requirements) gradually ceased operation. The majority of policyholders, contributions and financial reserves fell to a small minority (200-300) of today’s approximately 2,000 active pension funds.

{kind=link}

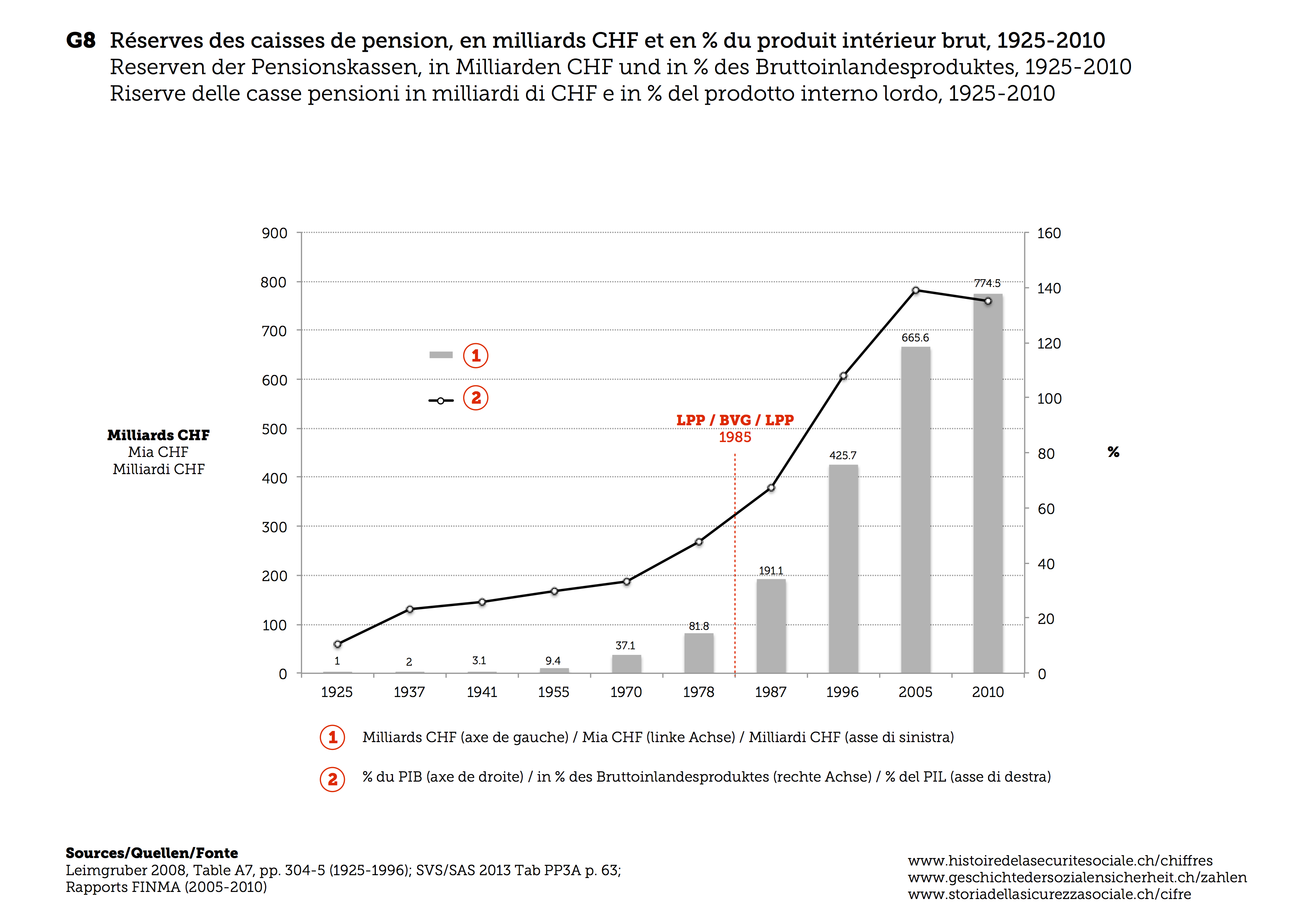

The pension funds have considerable reserves (F8). In 1978, these reserves amounted to almost half of Swiss gross domestic product. At the beginning of the 21st century, the funds’ reserves surpassed gross domestic product. The role of pension funds as institutional investors has gained substantial importance since the introduction of the BVG.

{kind=link}

Figures

F4 People aged 65 years and more as a percentage of the population, 1900-2010

F5 Number of recipients of AHV and pension funds benefits, 1925-2010

F7 Number of pension funds in the public and private sector, 1911-2004

F8 Pension funds reserves in billion francs and as a percentage of gross domestic product, 1925-2010

(12/2015)